The cost of living is expensive. Think back 20 or so years and see if you can remember what you thought it would cost to send your kids to college, or what the price of groceries would be. Are your utilities higher? Between currency devaluation and inflation, things cost much more now than what we expected.

I remember beginning to save for my kids’ education and thought that on the high end I’d need about $30k per child (I have 3). My first child cost $80k, second $60k, and the third is just starting; a bit of a short fall. Back in 1990, my out of state tuition for graduate school was $1800 per semester. Under graduate in state tuition is about $4500 per semester now. How do we make up for that? You work, you save, and you still can’t make ends meet. It gets to be frustrating. But, I am a trader of markets, and I have figured out how to cushion the blow.

I told you earlier that my first child cost $80k to go to college. He graduated high school in 2007. The dollar was weakening and I put the “college fund” into foreign currencies. By the end of 2009, I had paid for his tuition with currency conversion only (and interest since these were currency CD’s). I maintained the $100k I started with and used the proceeds of currency conversion to pay his expenses. I found a needle in a hay stack that made the short fall I was going to have almost a non-issue.

Many things I trade these days are not necessarily to make money, it is to pay for the things I buy or need to buy. I trade live cattle futures to pay for the meat on the table, and coffee for that cup of joe each day. Cotton for the clothes I wear, and some stocks because I bought stuff there and want my money back. I have found that the market is a great way of financing the many things I do and need. You can do it too.

Nobody likes to pay for utilities, but they are necessary. To help pay for the utilities, trading bond futures options seem to work well. Let’s discuss bond futures and their options a bit before we get to trading them.

[PDF] Options Trading Strategies Guide

This FREE strategy guide breaks down 11 specific options methods for a total game plan in any market condition!

Bond futures are a commodity that trades in 1/32 increments and are worth $1000 per point and $31.25 per tick (1000/32 = 31.25). It controls a $100,000, 30 year US treasury bond. It is traded by the bond price, not the interest rate of the bond, though, it is interest rate sensitive. So, if interest rates go higher, bond price goes lower, and if interest rates go lower, bond prices go higher. This is because of supply and demand.

Think about this, if I owned a bond with an interest rate of 5% and currently interest rates are at 2%, how many people want my bond? Lots, because they can get a better return with my bond, and so, the price of that bond is more expensive compared to the current bond. And if you switch that around, if I own a bond at 2% and current rates are at 5%, who wants my bond now? No one. So as interest rates increase, bond prices go down, and as the decrease, bond prices go up.

Bonds open at 17:00 CT and close at 16:00 CT. The price is displayed in decimal form or with a dash; 147.23, or 147-23, and sometimes 147’23. The 23 is in 32nd. So, the price is 147 and 23/32. If you multiply that by 1000, the bond is worth $147,718.75. Par value is $100,000, so in this case you would be paying a $47,718.75 premium. Economic news will affect bonds, as they look for inflationary (rising interest rates) or deflationary (falling interest rates) indications.

Options on bond futures trade in 64th increments. They trade as long as the bond futures are open and trading, so you can actually get out of your trade in the middle of the night, if need be. They are still $1000 per point but since they are half of a bond future tick, then they trade $15.625 per tick. The bond options are no different than equity options except the price per point/tick is different, and you are only controlling one bond futures contract, as opposed to 100 shares of stock. Since all futures are traded on margin, you will not have to have so much money to control the option contract. You will also notice that the strike prices are every half point on the bond options (32/64). You might want to write this down and go back through it a couple of times, but I believe we have enough to go on.

There are weekly options on the bonds. Some platforms only offer the monthly options, so beware of that. We are looking for income, so we will be selling the options to bring in premium. We want the option to deteriorate over the time of the option. So, if we sell a bond option at 16 (16/64) we will bring in $250. If we buy back the option at 5 (5/64), we pay $78.125 for it. The difference is the profit, 250-78.125 = $171.875. If we do this 2 to 3 times per month, this will generate $400 – $500 per month, per contract, to help pay the utilities.

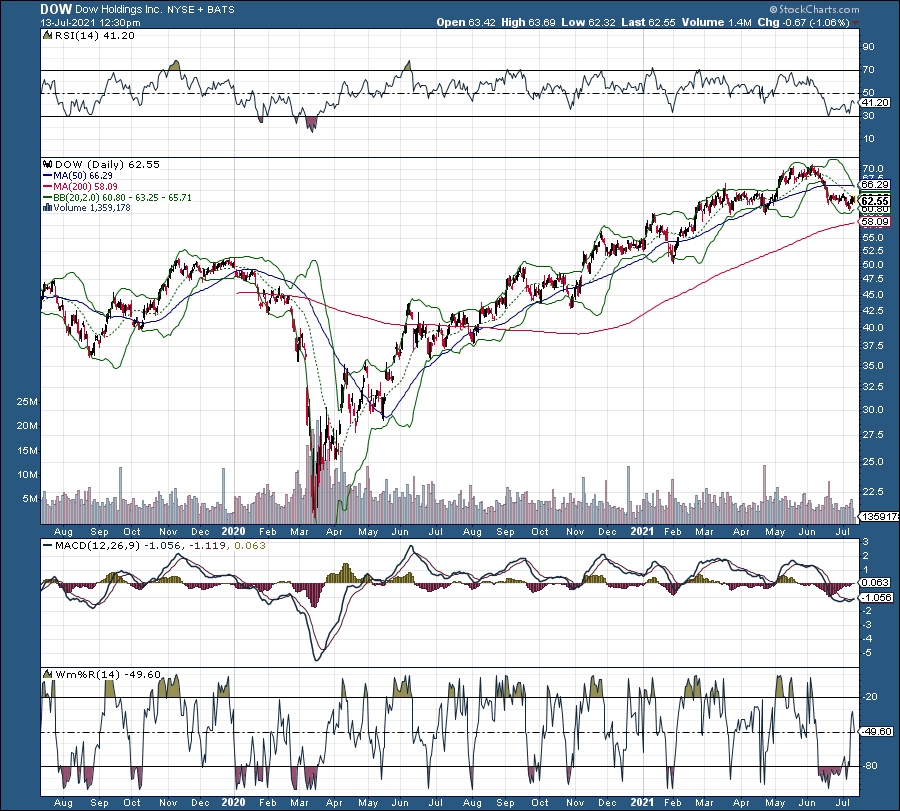

To set up the trade, first we don’t want to risk more than $300 per contract in any trade. So, if we sell an option at 16, then if it doubles or goes 19 ticks against us, then we will get out of the trade. If using weekly options, we will not be bringing in much premium, so we will look for something between 10 and 20 ticks on the options ($150 – $300), and look to get out between 0-5. Next, we need to look at the trend of bonds. Here is a daily chart on the bonds (USU17 September 2017, 30yr Treasury bond future):

The S1, S2, and S3 are support points on the chart. Notice bonds are in an uptrend. So, selling put options will be the safest play since bonds will have a tendency to go up. We will try to sell options at the support points. Of course, the closest support point will bring in the most premium (S1) and the furthest support point (S3) will bring in the least premium unless we go out further in time. If your platform only does monthly options, then I’d use the S3 point, but if using weekly options, use S1 or S2. Another thing to keep in mind, find out when the big economic news is coming out since bonds will react to it.

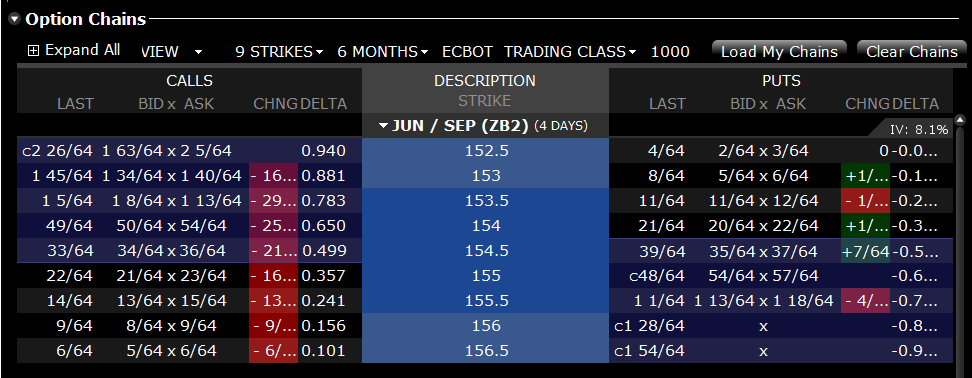

Look at the option chain below. Our S1 is around the 153 strike. The Jun 9 Put option is trading at 8/64. The 153.5 is at 11/64. The 153 is around the S1 on the chart and bonds will have to decline another point and a half to get to that strike. Let’s do the 153 strike. The current bid and offer are 11/64 – 12/64.

If we put an order to sell at 12/64 and get filled, we will bring in about $187.50. If today is Jun 5th and bonds are trading at 154-15, we will have to wait 4 days for the option to expire. As long as the bond futures stay above 143-00 then the option will lose value each day. If there is a big economic news day this week, we will need to either get out and take the profit we have, or be ready to exit if the bonds drop off because of the news.

For this trade, you will have to have a futures account with about $5000 in it. If you don’t have a futures account, another way of looking at this trade is by using TLT (20 yr. Treasury bond ETF). It too has weekly options, but selling naked puts may “cost” a little more since you will have to hold the put overnight and have a 50% margin on the value of the ETF. So, the question will arise, can you do a put spread? Yes. However, you want to do this is just fine. With the spreads, you may have to do multiple contracts to make up for the less premium being brought in, but they will work fine.

Doing this trade a couple of times a month can cushion the blow of the bills that come once a month. We can’t win them all, but remember, we will not risk anymore than $300 per contract. So, one loss will scratch one win for the most part. If you have never traded options on bonds, paper trade it for a couple of weeks to see how it goes. Once you get the hang of it, start paying some bills. Good luck trading.

THE SPECIAL OFFER

Sign up below to get a chapter of Tom Busby’s new best-selling eBook emailed to you daily!

ABOUT THE AUTHOR

Author: Geoffrey Smith, CEO & Chief Instructor

Company: Diversified Trading institute

Website: DTItrader.com

Services Offered: Trading Education, Trade Alerts, Trade Rooms, Software

Markets Covered: Stocks, Options, Futures, Day Trading, Swing Trading

An active trader and investor for 25+ years, Geof focuses in futures, equities and option trading including trading commodity option futures. Geof took an instrumental role in developing the DTI Method. The Platinum Experience core level classes took first place in SFO Magazine and Trader Planet’s STAR awards in the best trading courses category.